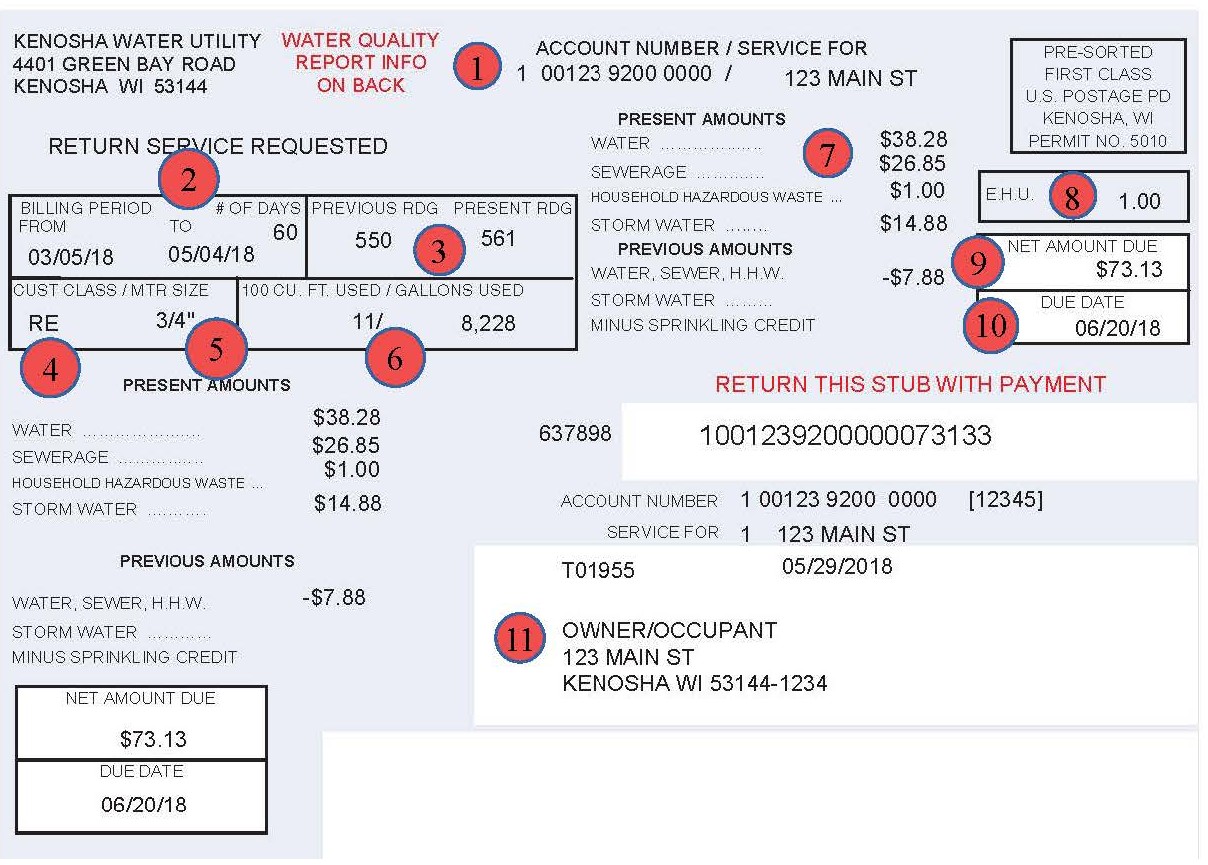

- Account Number

- Billing Period – The dates that the meter at your property was read. The utility performs actual readings and does not estimate consumption, except in unusual circumstances.

- Meter Readings - These readings are the hundred cubic feet of water that registered on the meter at the time it was read.

- Customer Class - RE - Residential CO - Commercial CR - Multi-Family PU - Public IN - Industrial PF - Frivate Fire

- Meter Size – The size of the meter determines the base charge for water, sewer, and public fire protection.

- 100 Cubic Feet Used – This is the volume of water that passed through the meter during the billing period. The meter measures the water in 100 Cubic Feet. 100 Cubic Feet is equal to 748 gallons. To determine the volume in gallons, multiple the volume in this box by 748. For example, 11 (100 cu ft) x 748 = 8,228 gallons.

- Water, Sewerage, HHW, Storm Water

- Water – Treated water consumed at property

- Sewerage – Based on the amount of water consumed. This is the cost to treat the wastewater before it is discharged back into Lake Michigan.

- Household Hazardous Waste (HHW) – A monthly service provided to residential customers to safely dispose of hazardous materials.

- Storm Water – Charges consist of a fixed base fee (charged to all parcels) and a variable fee based on EHU’s.

- Previous Amounts – The balance left from previous billing, including penalties

- Minus Sprinkling Credit – Residential customers who use a minimum of 10 ccft ( hundred cubic feet) bimonthly may be eligible for a sprinkling credit on three of their six bill cycles. The credit is calculated by the computer based on the excess usage for summer months that exceeds their normal average winter usage. The credit is for sewer volume charges in excess of the average winter usage in excess of 10 ccft.

- Equivalent Hydraulic Unit (EHU) – Represents a rate of water runoff, approximately 0.35 cubic feet per second (157 gallons per minute) from a typical residential property during a high intensity storm. For questions, please contact the City of Kenosha Public Works Department at (262) 653-4150.

- Net Amount Due – Previous amount plus the current bill amount.

- Due Date – Payment is due 20 days after a bill is rendered.

- Mailing Address – Bills are typically mailed to the property address that receives these services, unless requested otherwise by the property owner.